Estate Planning for Business Owners Texas: Tax Strategies to Protect Your Legacy

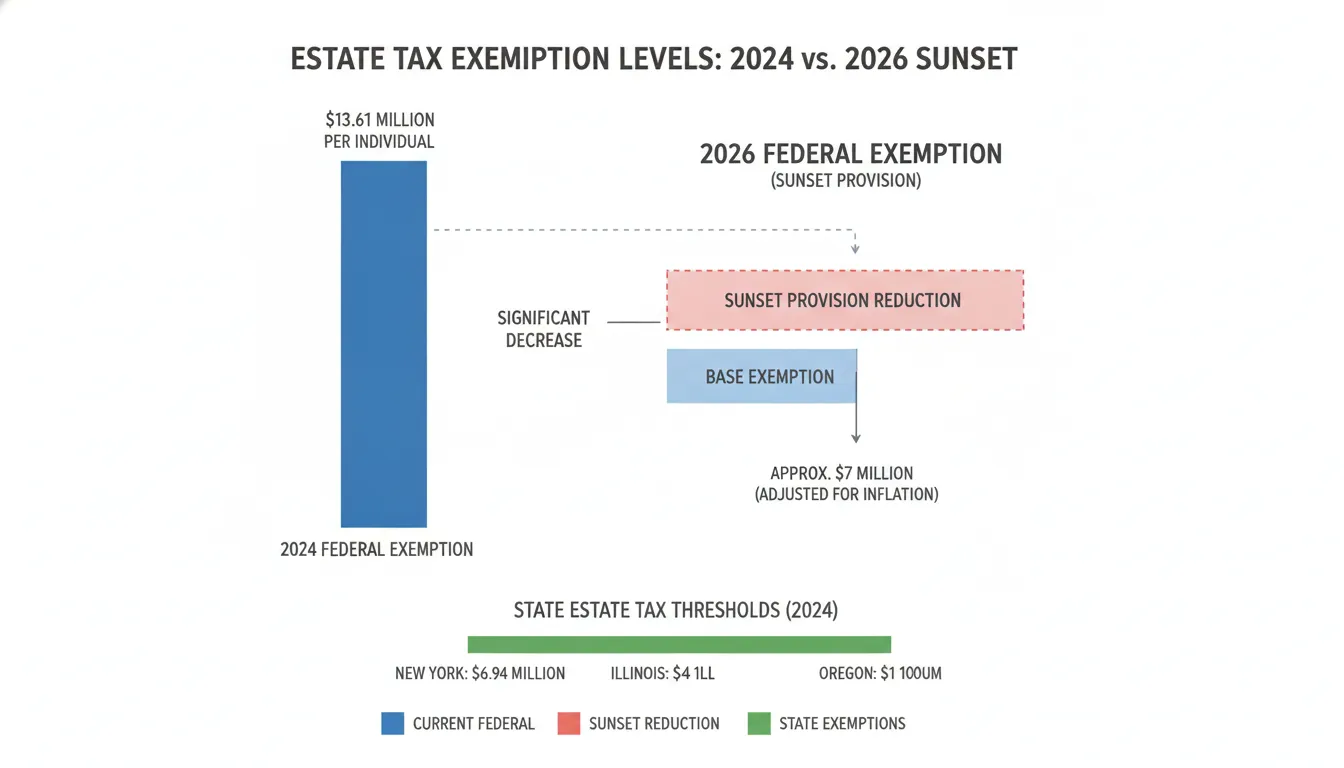

Texas does not impose a state estate tax, but federal exposure remains a major concern for business owners with substantial company value. The Tax Cuts and Jobs Act (TCJA) temporarily doubled the federal estate tax exemption to approximately $13.61 million per individual, but that provision sunsets on January 1, 2026. Without congressional action, the exemption will revert to approximately $5 million indexed for inflation, landing near $6 to $7 million. This impending reduction makes proactive estate planning for business owners Texas more urgent than ever.

Schedule a free estate planning consultation with Seamless today , our ABV-accredited CPAs will help you structure your business for the TCJA sunset and beyond.

Estate Planning For Business Owners Texas: How Does the Texas Estate Tax Landscape Affect Business Owners?

The absence of a Texas estate tax does not eliminate federal exposure, and the looming TCJA sunset in 2026 will cut the federal exemption roughly in half. Business owners with company valuations exceeding $6 to $7 million individually must act now to lock in current exemption levels through strategic gifting and trust structures.

Texas remains one of the most tax-friendly states for estate planning. There is no state-level estate tax, no inheritance tax, and no limitations on dynasty trusts that can span generations. However, the federal estate tax still applies to estates exceeding the exemption threshold. With the TCJA sunset approaching, the exemption for 2026 is projected to drop from approximately $13.61 million per person to roughly $6 to $7 million indexed for inflation. For a married couple, portability means the combined exemption could fall from approximately $27 million to roughly $13 to $14 million.

Federal estate tax mechanics for business interests

The federal estate tax applies to the fair market value of all assets owned at death, including closely held business interests. The IRS uses the willing-buyer-willing-seller standard to value private company stakes, and the top marginal rate reaches 40%. For a Texas business owner whose company is valued at $10 million, the estate tax liability could exceed $1.2 million if proper planning is not in place.

Protecting family wealth with the unified credit and portability

The unified credit shields a portion of every estate from tax. Portability allows a surviving spouse to retain any unused exemption from the deceased spouse, effectively doubling the protection for married couples. This becomes particularly valuable as the exemption shrinks in 2026. Strategic use of tax strategies to protect business value during this window can lock in today's higher exemption through lifetime gifts and grantor trusts.

Gift tax integration

Lifetime gifts reduce the available estate tax exemption dollar-for-dollar. Annual exclusion gifts (currently $18,000 per donee) and lifetime gifts to grantor trusts are essential tools for moving appreciation out of the taxable estate before the exemption contracts.

Why Does Business Valuation Matter for Estate Planning?

Accurate business valuation determines the tax liability your heirs will face and directly affects whether valuation discounts apply. Working with an ABV-accredited CPA ensures your valuation withstands IRS scrutiny and maximizes legitimate tax savings.

Your company is likely your largest single asset. The IRS requires a qualified appraisal for any closely held business interest included in a taxable estate. Seamless's business valuation practice, led by ABV-accredited CPAs including Brad Parker and Christopher O'Shell, provides court-tested reports that stand up to audit.

Three valuation approaches the IRS recognizes

The income approach projects future cash flows discounted to present value. The market approach compares your company to recent sales of similar businesses. The asset approach sums the fair market value of tangible and intangible assets minus liabilities. The appropriate method depends on your industry, growth stage, and ownership structure.

Valuation discounts that reduce taxable value

Two key discounts apply to business interests transferred to family members. A minority interest discount reflects the lack of control when a shareholder owns less than a controlling stake. A lack of marketability discount reflects the difficulty of selling a private company interest quickly. Combined, these discounts can reduce the taxable value of a transferred business interest by 25% to 40%, creating substantial estate tax savings when paired with tax planning for business owners.

Request a business valuation consultation with Seamless to determine your current estate tax exposure and discount opportunities before the 2026 exemption reduction.

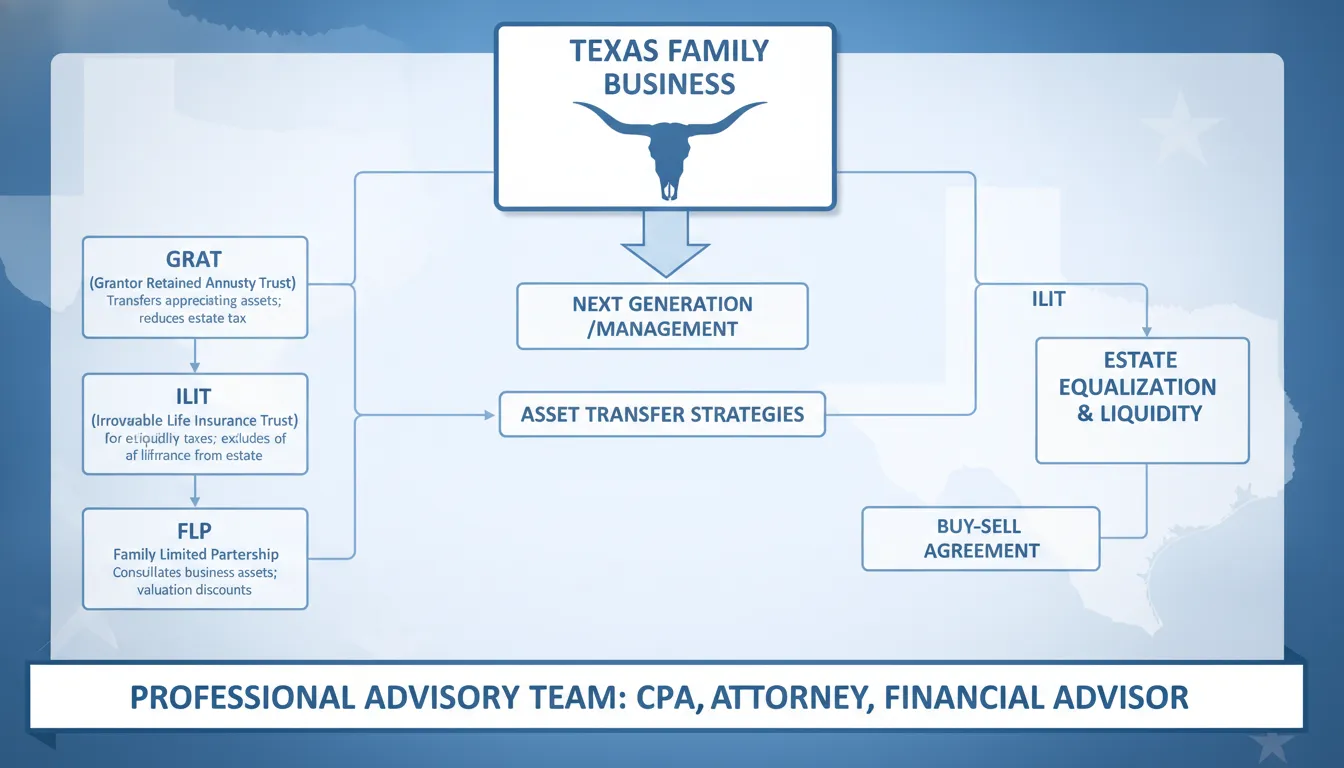

Using LLCs and Family Limited Partnerships to Protect Your Legacy

LLCs and Family Limited Partnerships (FLPs) provide asset protection, facilitate discounted wealth transfers, and bypass probate while you retain management control as the general partner.

Entity structure is the foundation of effective estate planning for business owners in Texas. An LLC separates personal assets from business liabilities. An FLP goes further by allowing you to gift limited partnership interests to family members at discounted values while retaining full control as the general partner.

How FLPs create tax-efficient wealth transfers

When you contribute business assets to an FLP and gift limited partnership interests to your children, those interests carry discounts for lack of control and lack of marketability. This means you can transfer more economic value within the annual gift tax exclusion or against your lifetime exemption. The IRS accepted this structure in Revenue Ruling 93-12, which recognized that minority interests in a family business are properly valued at a discount.

Avoiding Texas probate

Assets held in an LLC or FLP that are structured through a revocable living trust bypass Texas probate entirely. This keeps your business succession private, avoids court delays that can last six to twelve months, and ensures your chosen successor gains control immediately. For more on how these tax strategies protect business value, explore Seamless's corporate tax planning resources.

What Are GRATs, IDGTs, and Other Trust-Based Wealth Transfer Strategies?

Grantor Retained Annuity Trusts (GRATs) and Intentionally Defective Grantor Trusts (IDGTs) freeze the taxable value of appreciating business assets. Passing all future growth to heirs with minimal gift tax cost.

These sophisticated tools are especially valuable in the current rate environment. When interest rates rise, GRATs become more effective because the IRS assumes a lower rate of return (the Section 7520 rate). Making it easier for the actual asset growth to exceed the hurdle and pass to beneficiaries tax-free.

How a GRAT works

You transfer business shares into a trust and retain the right to receive fixed annuity payments for a term of years. If the assets outperform the IRS-assumed rate, the excess passes to your beneficiaries free of gift tax. For a rapidly growing Texas business, a GRAT can move millions in appreciation outside the taxable estate with minimal current gift tax cost.

The IDGT advantage

An IDGT is "defective" for income tax purposes, meaning you as the grantor pay the trust's income taxes. This allows the trust assets to grow undiminished by taxes, functioning as an additional tax-free gift to your heirs. You can sell business interests to the IDGT in exchange for a promissory note, freezing the value for estate tax purposes while retaining installment payments.

Combining trusts with valuation discounts

The most powerful estate planning strategy pairs trust structures with professional business valuations. When you contribute minority interests in a closely held business to a GRAT or IDGT, the discounted value allows you to leverage your gift tax exemption further. Seamless's ABV-accredited team provides the valuation reports necessary to support these structures under IRS scrutiny.

Life Insurance Trusts and Charitable Planning for Business Owners

Irrevocable Life Insurance Trusts (ILITs) remove policy proceeds from your taxable estate, providing tax-free liquidity for estate taxes. While Charitable Remainder Trusts (CRTs) convert appreciated assets into income streams with immediate tax benefits.

Why every business owner should consider an ILIT

Many business owners carry substantial life insurance to fund buy-sell agreements or provide family liquidity. If you own the policy personally, the death benefit is included in your taxable estate. An ILIT removes that benefit from your estate, giving your heirs cash to pay estate taxes, settle debts, or buy out co-owners without selling business assets.

Charitable trusts for income and legacy

A CRT lets you contribute appreciated business assets, receive an income stream for life or a term of years, and claim a charitable deduction. The trust sells the assets tax-free, reinvests the full proceeds, and pays you income. After the term ends, the remainder goes to your chosen charity. This structure is particularly effective for owners approaching exit who want to diversify while supporting philanthropic goals.

Business Succession Planning and Buy-Sell Agreements

A properly structured buy-sell agreement ensures your business transfers according to your wishes, provides liquidity for estate taxes, and prevents ownership disputes among heirs.

Cross-purchase vs. entity-purchase agreements

Two primary buy-sell structures exist for multi-owner businesses. A cross-purchase agreement has each co-owner buy life insurance on the others, providing the surviving owners with tax-free funds to purchase the deceased owner's shares. An entity-purchase (redemption) agreement has the business itself purchase the shares. The choice affects basis, control, and premium costs.

| Feature | Cross-Purchase | Entity-Purchase |

|---|---|---|

| Who buys the policy | Each co-owner | The business entity |

| Tax basis impact for survivors | Step-up in basis on purchased shares | No basis step-up; shares retained by entity |

| Number of policies needed | n (n-1) for n owners | One policy per owner |

| Control implications | Survivors increase ownership percentage | Survivors' percentage unchanged |

| Administrative complexity | Higher with multiple owners | Simpler to manage |

Funding the agreement

Life insurance remains the most reliable funding mechanism. The policy proceeds arrive income-tax-free and provide immediate liquidity. Sinking funds or installment notes can supplement insurance but introduce collection risk. Your estate planning for Texas business owners should coordinate the buy-sell structure with your overall wealth transfer objectives.

Your Estate Planning Roadmap: Next Steps for Texas Business Owners

With the TCJA sunset approaching in 2026, the optimal window for estate planning is now. A structured approach ensures you maximize current exemptions and implement the right trust and entity strategies.

- Obtain a professional business valuation from an ABV-accredited CPA to understand your current estate exposure.

- Assess your entity structure and determine whether an LLC or FLP provides optimal asset protection and transfer flexibility.

- Evaluate trust-based strategies including GRATs, IDGTs, or ILITs based on your business growth trajectory and family goals.

- Structure or update your buy-sell agreement with proper funding through life insurance held in an ILIT.

- Implement lifetime gifting to lock in current exemption levels before the 2026 sunset reduces them.

Frequently Asked Questions

What happens to a Texas business if the owner dies without an estate plan?

Without a plan, the business will go through Texas probate, which can last six to twelve months. Heirs may face disputes over control, and the business could be forced to liquidate to pay estate taxes. A comprehensive plan using trusts, buy-sell agreements, and proper beneficiary designations avoids these outcomes entirely.

How long does Texas probate take for a business, and can it be avoided?

Texas probate typically takes six months to a year for a business estate. It can be avoided entirely by holding business interests in a properly drafted revocable living trust or through an FLP structure designed to bypass probate. This keeps your succession private and gives your heirs immediate control.

Can a business owner lower the estate tax value of their company?

Yes. Minority interest discounts and lack of marketability discounts can reduce the taxable value of transferred business interests by 25% to 40%. These discounts must be supported by a qualified appraisal from an ABV-accredited CPA and are well-established under IRS revenue rulings and case law.

Why do business owners need a specialized estate plan instead of a simple will?

A simple will cannot address business-specific issues such as valuation discounts, buy-sell funding, control succession, or trust-based wealth transfer. Business owners face unique challenges including liquidity for estate taxes, minority shareholder treatment, and the TCJA sunset. All of which require coordinated planning with a CPA firm experienced in business valuation and tax strategy.

Ready to Protect Your Business Legacy?

The TCJA sunset in 2026 will cut the federal estate tax exemption roughly in half, making 2025 a critical window for Texas business owners to act. Seamless's team of ABV-accredited CPAs brings together business valuation expertise, tax strategy, and entity structuring in one coordinated plan.

Call (972) 830-2622 or schedule your estate planning consultation online , we will help you protect the legacy you have built.